ELBR is more responsive to repo speed changes, that can result in shorter lso are-pricing away from financing as compared to MCLR

- Bank loans try tied to a benchmark rates, which is the lower rates of which a lender normally lend.

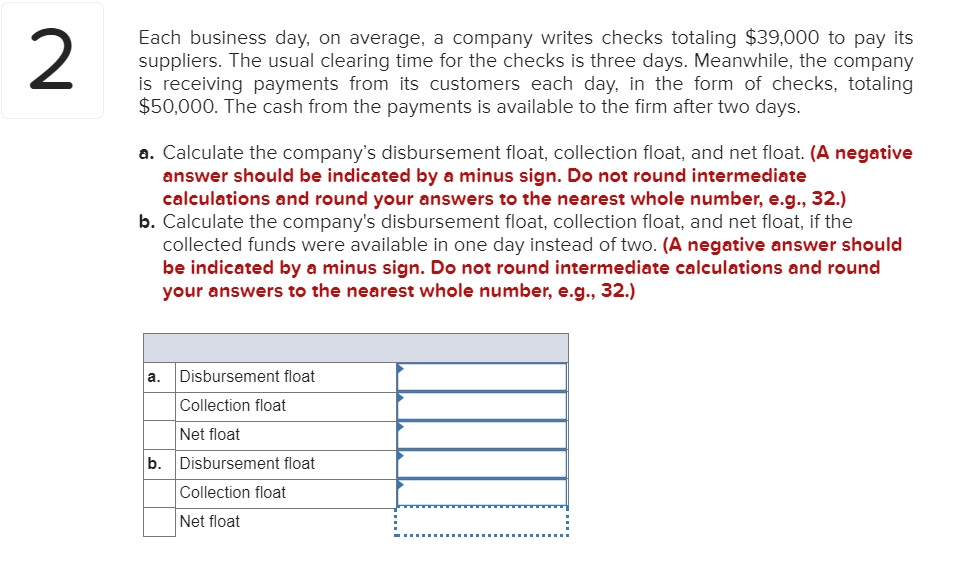

- The fresh new MCLR are designed to guarantee that rates offered by banking institutions moved easily as well as in combination towards the RBI’s repo rate moves.

- ELBR is far more attentive to repo rates transform, that may result in shorter lso are-rates away from financing as compared to MCLR.

The merger away from HDFC Ltd that have HDFC Financial provides proclaimed a great tall change inside the lending methodology having existing mortgage borrowers. For that reason, banking institutions have started transitioning borrowers in the current MCLR (Marginal Price of Lending Speed) so you’re able to ELBR (Additional Benchmark Financing Rate). So it change is vital getting individuals to understand, as you possibly can somewhat apply at the equated monthly instalments (EMIs), the entire focus paid back, and the financing tenure.

Loans was linked with a standard price, which is the reduced rate from which a lender can lend. Finance companies use a credit spread-over that it standard. Brand new spread is determined based on affairs for instance the borrower’s gender, revenue stream, credit score, and you will amount borrowed. The fresh standard and credit history means the final speed out of attract where that loan is given.

The newest MCLR, produced when you look at the 2016 of the Put aside Financial out of India (RBI), are meant to make sure that interest levels provided by banking institutions went easily as well as in combination on RBI’s repo speed moves. But not, this lending speed design did not reach their pri, this new RBI mandated most of the banks in order to hook up their retail financing costs so you can an external benchmark, for instance the repo speed, that is significantly more clear and you may beneficial so you can individuals.

HDFC Ltd-HDFC Financial merger: Exactly what distinctions home loan borrowers should become aware of in advance of shifting regarding MCLR to ELBR

Adhil Shetty, President out-of BankBazaar, says, The fresh new RBI produced MCLR 7 years back directly into alter the Foot Rates program. MCLR was calculated from the given individuals factors, such as the bank’s limited price of money, operating costs, and you can statutory put aside requirements. It mirrored the cost of borrowing with the lender and is actually supposed to be a great deal more tuned in to changes in the fresh new wider financial requirements versus Ft Price program. Finance companies lay the financing pricing for different types of fund (lenders, unsecured loans, and you can loans) by adding a spread or margin along side MCLR. The fresh pass on is set based on the borrower’s credit risk, loan tenure, or any other functional will cost you.”

An important factor to understand is the fact ELBR is more receptive to help you repo speed alter, that can produce less re also-cost out of money as compared to MCLR. Consequently one change in the newest repo rates have a tendency to now score shown smaller in your EMIs less than ELBR. Very, in the event that main financial cuts pricing, advantages will arrived at borrowers sooner or later, and you can alternatively, expands also are passed away reduced.

EBLR is produced to make the alert away from speed change so much more transparent, small, and you can tuned in to alterations in new larger benefit having people. In this instance, an interest rate was linked with an external benchmark price alternatively than just an inside rates set from the lender https://paydayloansconnecticut.com/pawcatuck/ by itself. This new RBI had into the 2019 introduced guidance that require finance companies to hook the credit pricing so you can outside standards for instance the policy repo price lay of the main lender, the brand new treasury statement prices, or any other markets-computed rates of interest,” said Shetty.

Present HDFC mortgage people may choose to switch to the fresh ELBR program cost-free. Yet not, consumers must gauge the gurus and possible issues just before transitioning. The new openness and you can quick changing character off ELBR may appear luring, however, think about, less rate posts may increase the weight when you look at the a growing focus circumstances. Rather than during the MCLR, where costs was reset all of the 6 otherwise 12 months, from inside the ELBR, alterations in the newest repo rate change the rates quickly.

Following RBI mandated banking institutions to hook up credit pricing to EBLR, of numerous finance companies transformed toward repo rate. The fresh new repo speed noticed of numerous updates – each other cuts and hikes – brought in a modification of brand new credit costs. Today, rates news started going on from inside the a much more foreseeable ways. The new MCLR, that was foreseeable in terms of the menstruation regarding rate updates (instance, just after for the 6 months), was in set because of the financial institutions and, ergo, more complicated so you can expect in terms of the quantum of your own price change. As well as, which have old standards, loan providers failed to give the rate slices so you can borrowers within exact same rates while the rate hikes. So it occurrence away from terrible policy signal, that the RBI enjoys lamented historically, remaining rates of interest at increased levels.

“That have EBLR lenders, rates posts are instantaneously passed away towards individuals. After losing so you’re able to six.fifty per cent before , lenders have increased to around nine per cent since the repo stands in the six.5 %. A reduced develops attended down seriously to step one.ninety percent on the qualified borrower, and so the lowest cost are in fact in the 8.forty percent variety,” told you Shetty.

So, in case your mortgage is related in order to MCLR and you may end up being expenses a major premium over the market costs. Therefore, you’ll be able to thought switching to an EBLR as the spread over the new repo rate might have been dropping, extra Shetty. The brand new borrowers try benefitting regarding all the way down give speed as compared to current ones. Before generally making this new switch, read the give rates accessible to both you and do your maths to know what kind of cash you will put away.

Shetty said, “If you’re a primary debtor which have a very high give (dos.5-step 3 per cent), then it are wise to refinance to some other repo-linked financing. The lower spreads remain repaired in the course of the borrowed funds. If the inflation are domesticated in the near future and also the repo rates drops, the brand new pricing do automatically belong to 8% again.”

If it is lowest as well as your interest was at level to your this new repo-linked financing, you ought to stick to the MCLR program to get rid of refinancing will set you back. If the, later, rates of interest fall, you can proceed to an effective repo-connected loan to profit from the faster signal out-of speed slices.

Ergo, borrowers is to very carefully determine their most recent financial factors, upcoming applicants or any other related products just before progressing away from MCLR to help you ELBR.

Leave a Reply